مقدمة

مع ما يقرب من مليوني بائع نشط يعملون على موقعها الإلكتروني، تُعد أمازون أكبر شركة تجارة إلكترونية في العالم. واليوم، تضم المنصة مزيجاً متنوعاً من الشركات الصغيرة التي لا تدر سوى بضع مئات من الدولارات شهرياً من عائدات المبيعات، والعلامات التجارية المعروفة التي تستخدم أمازون كواحدة من قنوات البيع العديدة الخاصة بها، والشركات الناجحة التي تم إنشاؤها في البداية بهدف بيع المنتجات على أمازون بشكل أساسي. العديد من بائعي أمازون المستقلين الذين تمكنوا من بناء عملية ناجحة على المنصة يتطلعون الآن إلى جني الأموال وبيع أعمالهم إلى إحدى شركات أمازون العديدة التي ظهرت في السوق في السنوات القليلة الماضية.

ولكن في حين أن هناك الكثير من الاهتمام من أصحاب الأعمال الذين يتطلعون إلى بيع عملياتهم إلى مجمّع أعمال، إلا أن هناك القليل جداً من المعلومات المتاحة للجمهور حول الشركات التي يرغب المجمّعون في النظر في الاستحواذ عليها والهيكل العام وشروط الصفقات التي يتفق عليها الأطراف عادةً. وفي الوقت نفسه، هناك العديد من المفاهيم الشائعة التي يعتقد البائعون على نطاق واسع أنها صحيحة دون وجود أدلة كافية تدعمها.

في ضوء هذه الظروف، تحدثت Nuoptima إلى أكثر من 20 شركة تجميع من أمازون، وجمعنا معلومات حول تفضيلات المجمّعين والتقييمات وهوامش الربح وهياكل الصفقات والعديد من العوامل الأخرى. سنقدم البيانات التي جمعناها ونناقش الاستنتاجات التي يمكن استخلاصها منها على مدار سلسلة من المقالات حول هذه المسألة. ستناقش مقالتنا الأولى العوامل المختلفة التي تنظر إليها شركات التجميع عند اختيار أهداف الاستحواذ.

فئات أمازون المفضلة والمستبعدة من قبل شركات التجميع

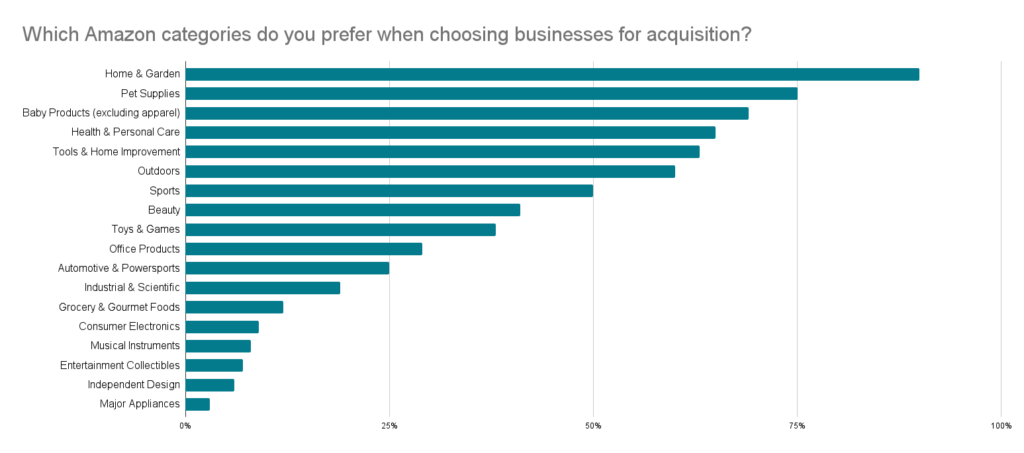

وفقاً للدراسة التي أجريناها، فإن غالبية شركات التجميع تتطلع إلى الاستحواذ على شركات في فئات المنزل والحديقة، ومستلزمات الحيوانات الأليفة، ومنتجات الأطفال، والصحة والعناية الشخصية، والأدوات وتحسين المنزل، والهواء الطلق، والرياضة، والجمال، والألعاب والألعاب. وهذا ليس مفاجئاً، لأن هذه الفئات من أكثر الفئات شعبية على المنصة بشكل عام. معظم المنتجات المباعة في هذه الفئات دائمة الخضرة ولا تحتاج إلى إعادة تصميمها بشكل متكرر للتكيف مع اتجاهات المستهلكين المتغيرة. بالإضافة إلى ذلك، هذه السلع ليس لها تواريخ انتهاء صلاحية قصيرة أو متطلبات تخزين معقدة، كما أنها لا تخضع لمعايير جودة صارمة تفرضها أمازون أو الجهات التنظيمية الحكومية.

تجدر الإشارة إلى أن مجمّعي أمازون مهتمون بشراء العلامات التجارية التي تصنع منتجات يكثر عليها الطلب والتي من المحتمل أن تظل مربحة وتستمر في تحقيق مبيعات لسنوات عديدة. هذا يعني أن البائعين الذين يقدمون منتجات في الفئات التي شهدت زيادة في شعبيتها منذ بداية جائحة كوفيد-19 هم في وضع جيد بشكل خاص للتفاوض على شروط استحواذ مواتية.

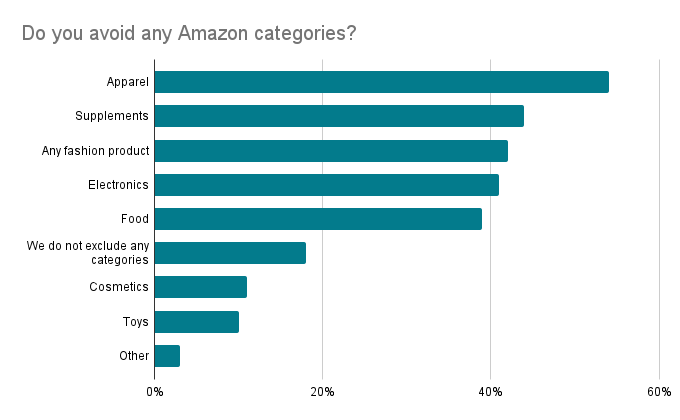

وفي الوقت نفسه، هناك العديد من فئات المنتجات التي تختار شركات التجميع تجنبها، على الأقل في الوقت الحالي. فوفقاً للدراسة التي أجريناها، ذكرت العديد من الشركات أنها لن تفكر في شراء العلامات التجارية التي تبيع الملابس والمكملات الغذائية والموضة والإلكترونيات والأطعمة والألعاب ومستحضرات التجميل. وتتطلب هذه المجموعات من المنتجات ابتكارًا مستمرًا وتغييرات في الأصناف، وتحتاج إلى الالتزام بإرشادات تنظيمية صارمة، أو أن تكون مدة صلاحيتها قصيرة. قد تحظر وكالة الصحة في المملكة المتحدة، MHRA، مكملاً غذائيًا في المملكة المتحدة وهو مقبول تمامًا في ألمانيا على سبيل المثال، مما يجعل من الصعب على المجمّع التوسع في استخدام نفس المنتج على مستوى العالم. الأجهزة الإلكترونية لها عيب اختلاف المقابس والمقابس في بعض البلدان. بالإضافة إلى ذلك، تهيمن على فئات الملابس ومستحضرات التجميل بشكل أساسي العلامات التجارية الوطنية وحتى العالمية المعروفة، مما يزيد من صعوبة جذب البائعين للعملاء إلى قوائمهم.

ومن المثير للاهتمام أن ما يقرب من 201 ت3 ت3 من الذين تمت مقابلتهم ذكروا أنهم لا يستبعدون أي فئات من النظر، مما يشير إلى أن العديد من العوامل الأخرى تؤثر على قرار الاستحواذ على شركة ما.

أنواع الشركات التي تستحوذ عليها شركات التجميع عادةً

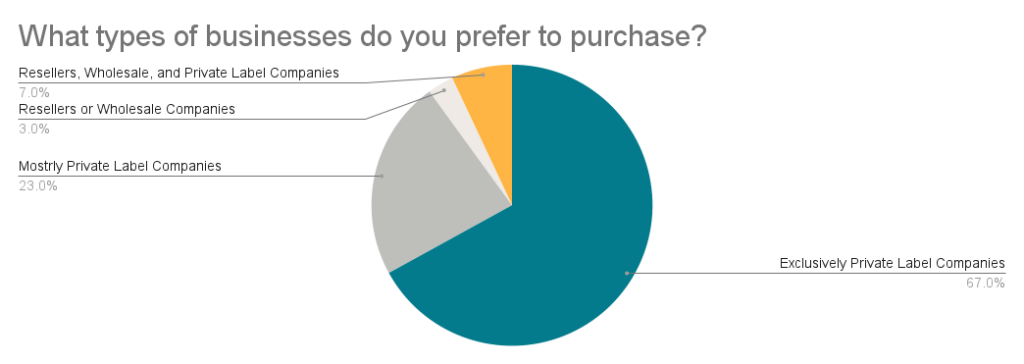

أشار غالبية من تمت مقابلتهم إلى أنهم لا يفكرون إلا في الاستحواذ على شركات العلامات الخاصة. من ناحية أخرى، ذكر 3% فقط من المجيبين أنهم منفتحون على شراء شركات إعادة البيع أو شركات البيع بالجملة. وقال 7% من المجيبين الآخرين أنهم يفكرون في شراء جميع أنواع الشركات الثلاثة.

هناك سبب مهم لهذا الاتجاه، حيث تتمتع شركات العلامات التجارية الخاصة بالعديد من المزايا التجارية مقارنةً بالبائعين وبائعي الجملة. فعلى عكس البائعين بالجملة والبائعين الموزعين بالجملة، تمتلك شركات العلامات التجارية الخاصة منتجاتها الفريدة من نوعها. وبما أنهم يبيعون منتجات حصرية، يمكن لهذه الشركات التقدم بطلب للحصول على علامة تجارية قابلة للتنفيذ، والانضمام إلى برنامج أمازون لتسجيل العلامات التجاريةوإنشاء قوائم المنتجات الخاصة بهم، وتجميع المراجعات وتوليد أصول قيمة أخرى.

وفي الوقت نفسه، يعتمد البائعون وبائعو الجملة اعتماداً كلياً على موردي منتجاتهم، الذين قد يتوقفون عن توفير المخزون في أي وقت. بالإضافة إلى ذلك، غالبًا ما يواجه البائعون غير المصرح لهم وشركات البيع بالجملة شكاوى الملكية الفكرية من العلامات التجارية، مما قد يؤدي إلى نفقات قانونية كبيرة. من ناحية أخرى، قد يكون المجمّعون على استعداد للنظر في شراء بائعين حصريين مع عقود قوية طويلة الأجل مع أصحاب العلامات التجارية.

المعايير الجغرافية التي تؤثر على عملية اتخاذ القرار خلال عمليات الاستحواذ على علامة أمازون التجارية

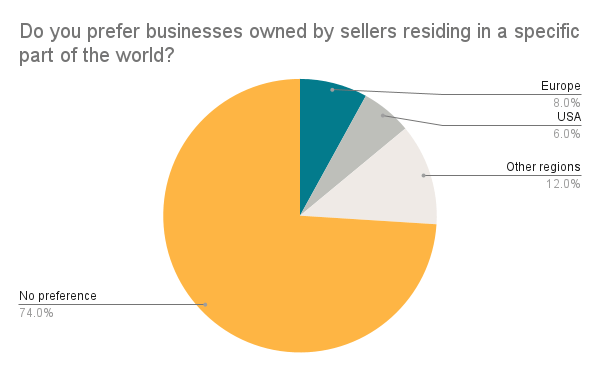

يعتقد العديد من بائعي أمازون والاستشاريين وخبراء الصناعة أن المجمّعين لا يشترون إلا الشركات الموجودة في الولايات المتحدة الأمريكية. ومع ذلك، تدحض محادثاتنا هذه الفكرة، حيث تُظهر أن أكثر من 70% من المجمّعين ليس لديهم تفضيل لموقع الشركة التي يخططون لشرائها. ولهذه الظاهرة تفسير بسيط، حيث إن معظم المشترين لا يشترون الكيان التجاري. وبدلاً من ذلك، فإنهم يستحوذون على أصول الشركة، والتي غالبًا ما تتضمن حسابات أمازون، وقوائم المنتجات، وبراءات الاختراع، والعلامات التجارية، والعلامات التجارية، والعلامات التجارية، والمخزون، والعقود مع الموردين، ومشغلي الخدمات اللوجستية، وما إلى ذلك.

وفي الوقت نفسه، فإن معظم المشترين الذين لديهم تفضيل فيما يتعلق بالموقع الجغرافي لشركة البائع يذكرون أن ذلك يرجع إلى قربهم الجغرافي من البائع. يساعد التواجد في نفس المنطقة أو البلد الذي يقع فيه البائع على تبسيط المفاوضات ويسمح للمجمّعين بالتواصل مع أصحاب الأعمال مباشرةً دون إشراك أطراف ثالثة.

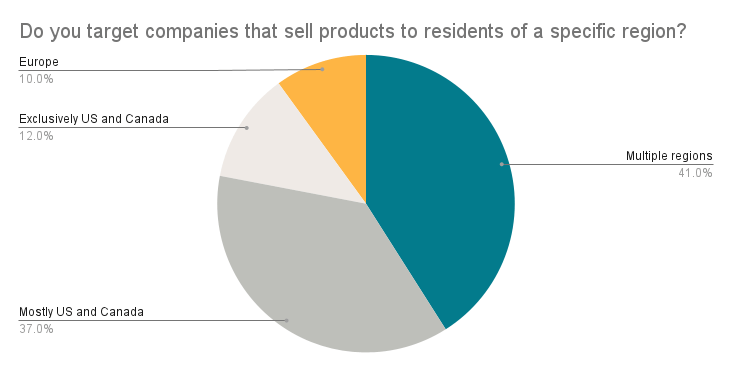

وفقًا لنتائج دراستنا، تفضل معظم الشركات التي تتطلع إلى الاستحواذ على علامات أمازون التجارية شراء شركات تعمل في مناطق متعددة حول العالم أو في الولايات المتحدة وكندا. فقد ذكر 12% فقط من المشاركين في الدراسة أنهم لا يفكرون إلا في الشركات التي يقع مقرها في الولايات المتحدة أو كندا، وذكر 10% من المشاركين أنهم يفضلون الاستحواذ على الشركات التي تخدم العملاء الأوروبيين فقط.

قد تكون هذه النتائج مفاجئة لبعض البائعين الذين يعتقدون أن تشغيل نشاط تجاري في منطقة واحدة فقط يضعهم في وضع غير مواتٍ مع المشترين المحتملين. ومع ذلك، يرى العديد من المجمّعين أن هذه فرصة لتوسيع نطاق العمل بسرعة في أسواق جديدة، والاستفادة من نجاح العلامة التجارية في السوق الأصلي لكسب العملاء والتغلب على المنافسة. بالإضافة إلى أن العديد من المشترين يفضلون شراء العلامات التجارية العاملة في الولايات المتحدة وكندا بسبب الحجم الهائل لقطاع التجارة الإلكترونية وقوته في هذه البلدان.

عوامل أخرى تؤخذ في الاعتبار عند تقييم أهداف الاستحواذ

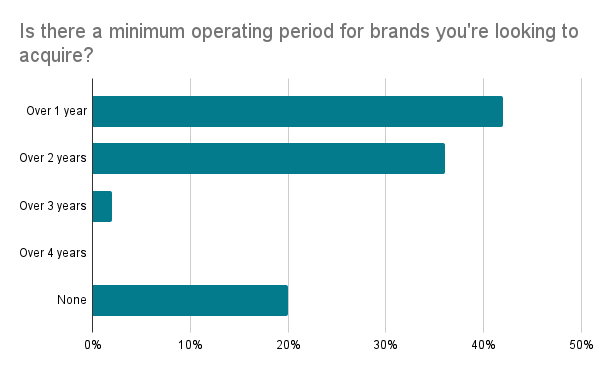

في حين يفترض بعض بائعي أمازون أن المجمّعين يعتبرون فترة التشغيل التاريخية الطويلة ميزة لهم، إلا أن هذا أبعد ما يكون عن الحقيقة. فوفقاً لمحادثاتنا، يفضل أكثر من 40% من المشترين شراء الشركات التي تعمل منذ عام واحد على الأقل. ويختار ما يزيد قليلاً عن 35% من المشترين الشركات التي تعمل لمدة لا تقل عن عامين، ولا يوجد لدى 20% من المجمّعين حد أدنى محدد لفترة التشغيل.

يمكن تفسير هذه البيانات بسهولة من خلال حقيقة أن شركات التجميع ترغب في الاستحواذ على الشركات التي يمكن أن تنمو بسرعة نسبياً. وإذا كانت الشركة تعمل منذ عدة سنوات، فقد تكون قد تجاوزت بالفعل فترة نموها. وفي الوقت نفسه، فإن الحد الأدنى لفترة التشغيل القصيرة يمكن أن يساعد المشترين على ضمان أن ينظروا فقط في الشركات التي لديها أصول كافية لجعل عملية الاستحواذ عليها جديرة بالاهتمام. وتشمل هذه الأصول عادةً المنتجات والقوائم والمراجعات والعلامات التجارية وما إلى ذلك.

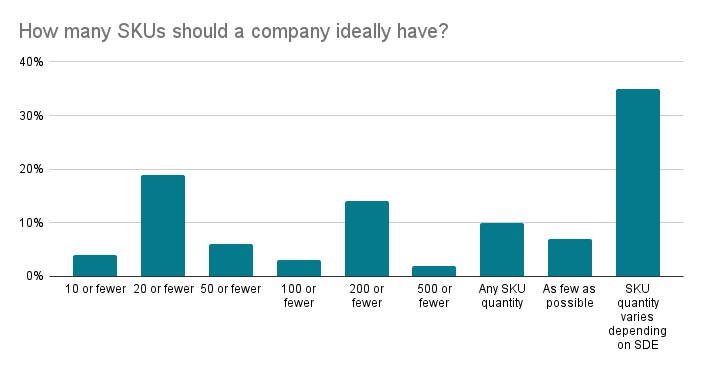

تُظهر البيانات الواردة في الرسم البياني أعلاه أنه عندما يتعلق الأمر بعدد وحدات حفظ المخزون لدى بائع أمازون، فإن تفضيلات المجمّعين المختلفين تتفاوت بشكل كبير. قد يعتمد هذا على موارد المشتري، وعدد الأشخاص الذين يمكن تخصيصهم لإدارة المتجر الذي تم الاستحواذ عليه حديثاً، ومقدار الخبرة التي يتمتع بها المجمع في الصناعة، وما إلى ذلك. ومع ذلك، ذكرت نسبة كبيرة من جميع الأشخاص الذين تمت مقابلتهم أن عدد وحدات حفظ المخزون ليس مهمًا بطبيعته. وبدلاً من ذلك، فإن ما يهم أكثر هو نسبة وحدات التخزين المجمعة لكل وحدة تخزين.

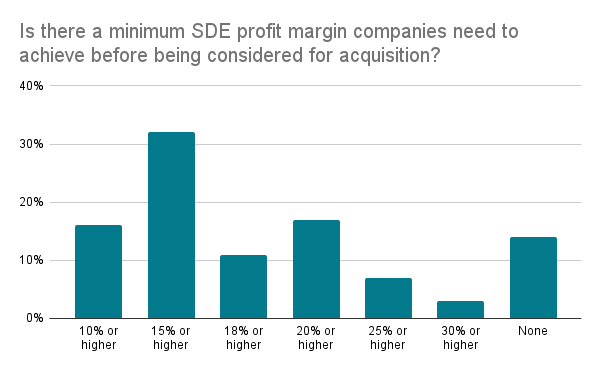

ووفقًا لنتائج دراستنا القائمة على المحادثات، فإن أكثر من 30% من مجمّعي أمازون على استعداد للنظر في الاستحواذ على شركة لديها هامش ربحية لا يقل عن 15%. في حين أن هذا الرقم منخفض نسبيًا، إلا أنه يمكن تبريره بأن المشترين يتوقعون أن يكونوا قادرين على تحسين الأعمال وزيادة هامش الربح. من المهم أيضًا ملاحظة أن الشركات ذات هوامش الربح المنخفضة عادةً ما تكون أرخص في الاستحواذ عليها، مما يجعلها أكثر جاذبية للمشترين.

الاستنتاجات

اليوم، تبحث معظم شركات التجميع في أمازون بنشاط عن شركات للاستحواذ عليها وإضافتها إلى شبكتها. تميل الشركات التي تبيع منتجات شائعة دائمة الخضرة دون قيود تنظيمية إلى أن تكون الخيارات الأكثر شعبية. بالإضافة إلى ذلك، تبحث معظم شركات التجميع عن الشركات التي تبيع منتجات في الولايات المتحدة وكندا أو مناطق متعددة ومتنوعة. وفي الوقت نفسه، لا يهم موقع الشركة كثيراً، لأن المشترين عادةً ما يستحوذون على أصول الشركة وليس الكيان القانوني نفسه. الشركات ذات العلامات الخاصة هي الخيار المفضل للمشترين، لأنها تتمتع بأكبر قدر من الاستقرار والنجاح على المدى الطويل. وبشكل عام، يهتم المجمّعون بشدة بالاستحواذ على الشركات التي يمكنهم تحسينها وتنميتها بشكل كبير.